Oct 8, 2025

Learn how to manage restaurant insurance cost effectively. Discover key strategies to save without sacrificing coverage.

Let's cut to the chase: The typical restaurant insurance cost is between $63 and $214 per month. That figure can vary based on your location, size, and claims history. Think of it as a non-negotiable line item, right alongside payroll and food costs.

An insurer's quote isn't a random number. It's calculated based on your restaurant's unique risks, digging into metrics like annual revenue and total payroll to land on your final premium. A higher payroll often means a higher workers' compensation premium because it signals more employee activity, increasing the chance of an on-the-job injury.

This is why a firm grip on your financials is critical, not just for managing your restaurant's profit margin, but for getting the right insurance at a fair price. This infographic shows how costs compare and what a typical policy includes.

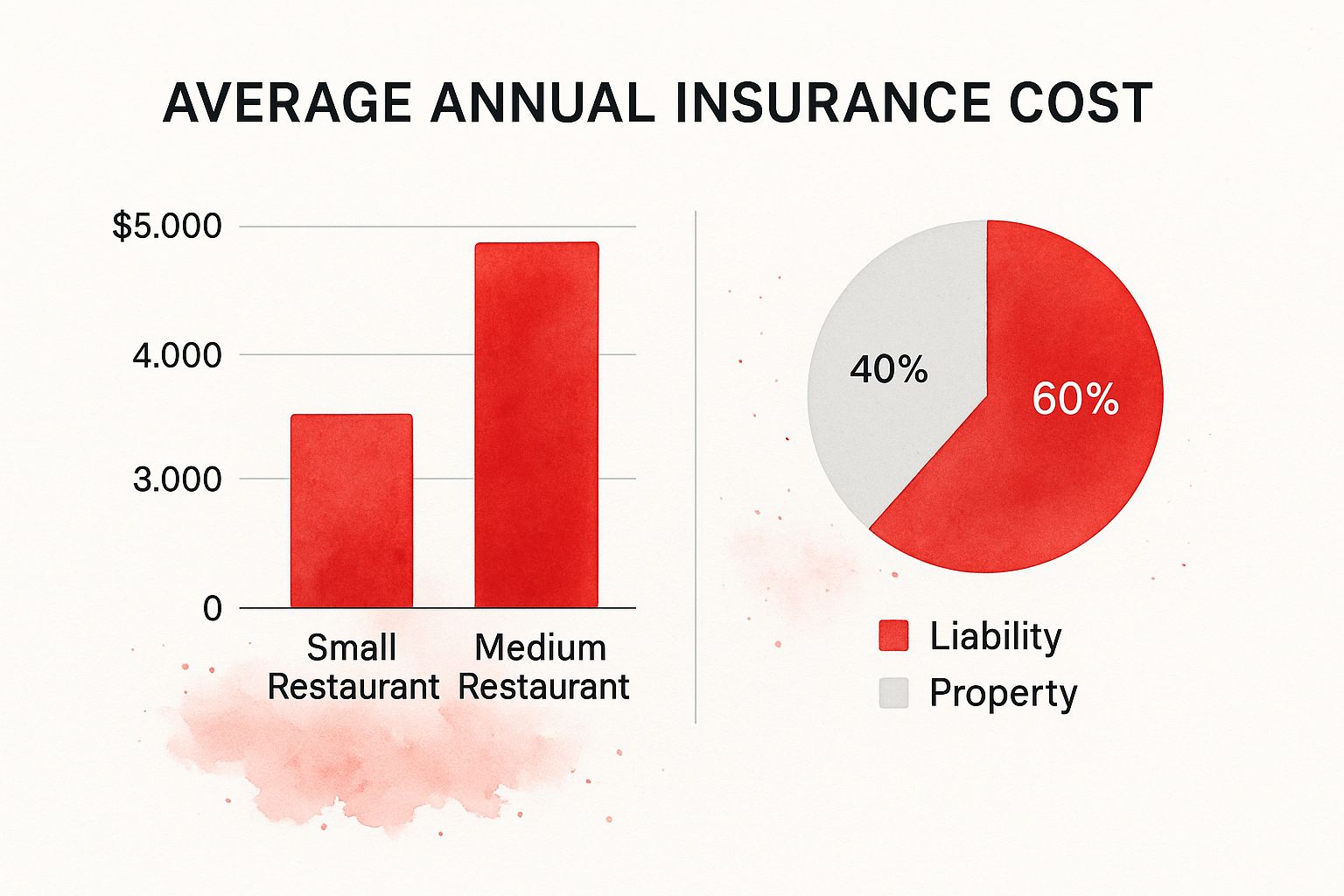

Liability coverage usually takes the biggest slice of the pie, reflecting the high risk of customer slips, falls, or other incidents.

To help you see how these pieces fit, here’s a table outlining what a small restaurant might pay.

Let's look at a small, independent restaurant with two employees, $150,000 in annual payroll, and $300,000 in annual revenue. A comprehensive policy would likely have coverage limits of $1 million per incident and a $2 million annual total.

For many owners, the most valuable part of their policy is Business Interruption coverage. This replaces lost income if a fire, storm, or equipment failure forces you to shut down. It's easy to overlook until you desperately need it. To understand its pricing, it’s worth reading a specific guide on business interruption insurance cost.

Did an insurance quote make you do a double-take? You're not alone. That quote isn't an arbitrary number; it’s a story about the specific risks an underwriter sees in your restaurant.

An insurer is just calculating the odds of a claim. A small cafe that closes at 3 p.m. has a completely different risk profile than a downtown bar with live music until 2 a.m. The first step to controlling your insurance costs is understanding what they see.

Insurers dig into the nitty-gritty of your operations. Every factor can nudge your premium up or down.

Here are the key areas underwriters focus on:

Your address and business history also play a massive role. Your claims history is like a credit score for your business. Several claims in the past three to five years signals higher risk. A clean record can lead to better rates.

Your location is also critical. A restaurant in a busy city with high foot traffic and higher crime rates will almost always pay more than a similar spot in a suburb.

While your individual costs might feel high, global commercial insurance rates have been declining lately due to more competition among insurers. To see how these trends are playing out, you can read more about recent insurance rate shifts.

Ultimately, your quote is a reflection of your risks. Pinpoint your biggest risk factors to start addressing them and prove to insurers that your restaurant is a safe bet.

Insurance policies can feel like they're written in another language. Let's cut through the noise and focus on the must-have coverages that form your restaurant's safety net. These are the non-negotiables that protect you from the most common and costly risks. Getting these right is as important as any step on a checklist for opening a restaurant.

This is your first line of defense. General Liability protects you from claims of bodily injury or property damage to third parties, like customers. It’s the policy for the classic slip-and-fall incident.

Your restaurant is full of valuable physical assets. Commercial Property Insurance protects the building, kitchen equipment, furniture, and inventory from events like fire, theft, or storm damage.

A kitchen fire can cause hundreds of thousands of dollars in damage in minutes. Property insurance is what allows a restaurant to rebuild instead of closing for good.

Your team is your greatest asset, and protecting them is legally required in most states. Workers' Compensation covers medical expenses and lost wages for employees injured on the job.

If you serve alcohol, this coverage is not optional. General liability policies almost always exclude alcohol-related incidents. Liquor Liability Insurance protects your business against claims caused by an intoxicated patron. If you over-serve a customer who then causes an accident, your restaurant could be held liable. This policy handles those unique risks.

Paying for insurance is a necessary cost, but that doesn't mean you have to accept the first quote. A proactive approach to safety and risk management can directly lower your restaurant insurance cost. It shows underwriters you’re a smart, low-risk operator.

Small, consistent actions prove a commitment to safety that insurers reward with better premiums.

The most effective way to cut insurance costs is to reduce the chance of a claim.

Beyond adjusting coverage, implementing robust asset protection strategies can make your entire business less vulnerable.

Once your safety protocols are solid, focus on finding the right policy and partner.

A Business Owner's Policy (BOP) is often the most cost-effective route. A BOP bundles essential coverages like General Liability and Commercial Property into a single, affordable package. It simplifies paperwork and usually includes a discount.

Seek out an independent insurance agent who specializes in the restaurant industry. A generalist won't understand the unique risks you face and won't have access to the niche carriers that offer the best rates.

Your POS can also help by providing detailed sales reports to track inventory and alcohol sales—key data for insurers. Understanding how the right restaurant POS system can transform your business operations can reveal new ways to protect your business.

The insurance market is always in motion, and many owners are feeling the pressure of rising costs. Understanding what's happening helps you anticipate changes so you aren’t blindsided by a massive rate hike at renewal.

A few key forces are making insurance trickier for restaurants. Inflation hits every corner of your business, and insurance is no different. When the cost to rebuild a kitchen or settle a liability claim goes up, premiums follow.

Another driver is "social inflation," a term for the ballooning cost of legal claims fueled by bigger jury awards. A simple slip-and-fall that might have settled for a predictable amount years ago could now lead to a multi-million-dollar verdict. Insurers are pricing that new risk into everyone's policies.

These aren't abstract concepts—they directly impact your next insurance quote. Insurers are baking this new reality into their rates.

As premiums climb, more restaurants are ditching insurance completely. It’s a massive gamble that a growing number of owners feel forced to take.

Recent numbers show that only 62% of restaurant owners reported having business insurance, a steep drop from 71% the year before. The share of uninsured restaurants shot up from 29% to 38% in a single year. You can discover more about these commercial insurance trends to see how widespread this is.

This hurts everyone. When fewer businesses pay into the insurance pool, the risk is spread across a smaller group, which can push premiums even higher for those who stay covered. It’s a vicious cycle. Knowing these forces exist helps you focus on what you can control—making your restaurant as safe and low-risk as possible.

Here are the most common questions we hear from restaurant owners.

A small, independent restaurant can expect a monthly premium between $80 and $250. This covers essentials like general liability and property insurance. A Business Owner's Policy (BOP), which most small restaurants get, averages around $251 per month. A BOP is usually the most cost-effective route, bundling critical coverages at a discounted rate.

Yes. In nearly every state, if you have employees, you are legally required to have workers' compensation insurance. It covers medical bills and lost wages for on-the-job injuries and, crucially, shields you from being sued by an injured employee—a lawsuit that could easily shut you down.

Think of a Business Owner's Policy (BOP) as an insurance combo meal. It bundles the two most critical coverages:

Buying a BOP is almost always cheaper than getting these policies separately and ensures you don't have major gaps in your coverage.

A high quote is a direct reflection of your specific risk level. Figuring out what's driving that number up is the first step to bringing it down.

Your insurance cost is a risk calculation. A late-night bar with live music is a totally different animal than a quiet cafe that closes at 3 p.m. Insurers price that difference.

Common reasons for high premiums include:

Once you pinpoint your biggest risk factors, you can implement safety measures to tackle them and prove to insurers you deserve a better rate.

Managing risk is one piece of the puzzle. Running a tight ship requires tools that give you real control.

Peppr offers a restaurant POS and growth solutions designed by people who’ve worked in the trenches, giving you everything from handhelds to KDS to commission-free ordering. See how you can streamline your operations.